Drivers in Michigan are due for some sweet relief as sweeping insurance legislation takes effect on July 2, 2020.

Michigan residents, read on! You could qualify for cheap auto insurance rates this summer.

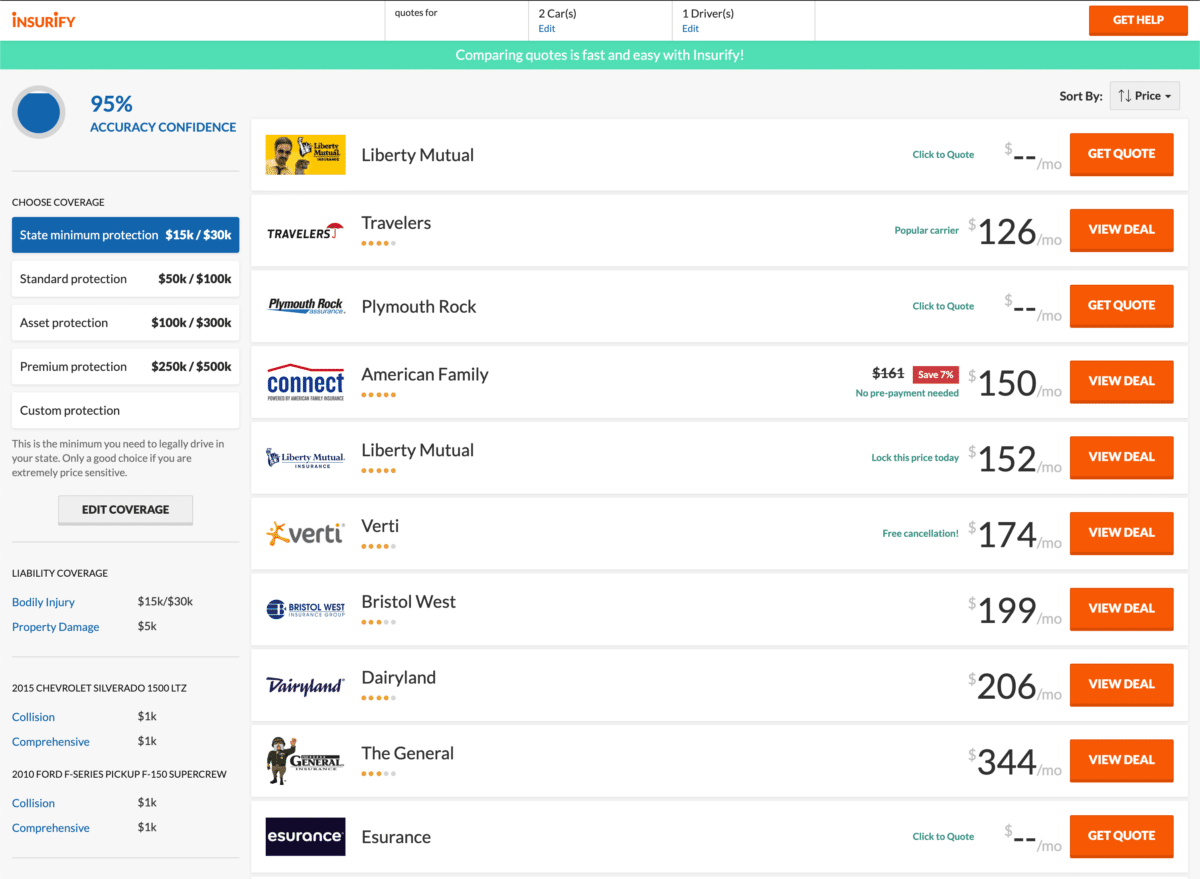

Score savings on car insurance with Insurify

How does Michigan’s auto insurance reform affect me?

Michigan’s historic, bipartisan auto insurance reform laws seek to reduce auto insurance rates for everyday drivers and strengthen consumer protections. That means less money out of your pocket and more accountability after an accident or a claim.

Each element of Michigan’s new auto insurance law applies to policies issued after July 1, 2020. This means if you bought an auto insurance policy that takes effect on or before July 1, these rule changes won’t apply to this policy period. But any policy issued on July 2, 2020, or later must abide by these changes.

Some of these new regulations apply to insurance companies. Others apply to you, and the amount of coverage you select when buying a new auto insurance policy. All in all, however, many Michigan drivers should enjoy lower car insurance rates and premiums.

Shopping for a new auto insurance policy this summer? Use Insurify to compare auto insurance quotes from top companies in mere minutes. Compare real, ready-to-buy quotes, providers, and discounts all in one place. No games, no hassle. 100% free.

Score savings on car insurance with Insurify

Here’s what Michiganders can expect to see change for their auto insurance plans:

1. Personal Injury Protection (PIP) changes: no-fault auto insurance reform

Beginning July 2, 2020, Michigan drivers will have options when it comes to coverage levels for minimum liability insurance requirements. To lower auto insurance costs for Michigan drivers, Gov. Gretchen Whitmer passed legislation strengthening consumer protections for MI drivers. This improved no-fault system will allow drivers to choose their coverage levels and, in turn, cut costs dramatically.

For the first time, drivers will have a choice in the level of medical coverage attached to their auto insurance policy. Drivers can choose from the following Personal Injury Protection (PIP) coverage options:

- Unlimited PIP coverage

- $500,000 coverage limit

- $250,000 coverage limit

- $250,000 coverage limit with PIP medical exclusion(s). Applies to drivers who already have private healthcare coverage that covers injuries related to a car accident, or those whose spouse or household relatives have a qualifying healthcare plan that covers injuries related to an auto accident.

- $50,000 coverage limit. Only applies to Medicaid recipients or those whose spouse or household relatives have a qualifying health plan that covers injuries related to a car accident.

- No PIP coverage. Only applies if drivers, their spouses, and all household relatives have Medicare or a qualified health insurance plan.

2. Reduction in PIP premium rates.

Michigan drivers will also be happy to know that, starting July 2, the state will mandate insurance companies to reduce PIP premium rates for at least eight years.

The lower coverage you receive, the higher the average price reduction.

- Unlimited personal injury protection would receive on average a 10% reduction

- $500,000 in coverage would reduce on average by 20%

- $250,000 in coverage would reduce on average by 35%

- $50,000 in coverage would reduce on average by 45%

- Individuals with Medicare or qualified health insurance could opt out and receive a 100% rate reduction on certain portions of PIP, depending on their individual circumstances. The Michigan Catastrophic Claims Association (MCCA) deficit fee would still apply (MCCA has announced the deficit fee is $0 for 2020).

Auto insurers and medical providers will now follow a fee schedule as a means of cost control. Overall, this will make PIP medical coverage premiums lower for policyholders without affecting the quality of service.

The MCCA will lower its per-vehicle assessment in response to this new law. If a member insurance company pays out a PIP medical cost over $580,000, the MCCA will still reimburse the company, but at a lower expense, saving drivers “at least $120 per car.” Drivers who choose any coverage under unlimited PIP medical coverage will not have to pay any assessment fee to MCCA.

3. Some elements of your personal profile won’t count against you.

Effective July 2, some personal factors will NO LONGER be used to set insurance rates for personal policies. These variables include:

- Sex

- Marital status

- Homeownership status

- Credit score

- Education level

- Occupation

- ZIP code

What does this mean for you? It means that your driving history will primarily set your auto insurance rates. Insurance providers can’t hike up your rates on a discriminatory basis when it comes to your neighborhood or whether or not you finished your degree. That’s a massive win for drivers all across the state.

4. Increases to minimum liability coverage limits.

The state will increase minimum liability coverage limits to $50,000 per person and $100,000 per accident. If you do not choose this new minimum liability coverage limit, your policy will default to $250,000 per person and $500,000 per accident. Policyholders will be sent a new selection form at each renewal to opt into lower coverage limits.

What does this mean for you? You’re protected from other claims by injured people in you’re at fault for an accident. Your insurance company must now offer you a higher bodily injury coverage payout, even if you’re just driving with state minimum liability coverage.

5. More consumer protection.

Michigan has established a fraud investigation unity that will work with the Attorney General to crack down on criminal or fraudulent activity in the insurance industry. Less auto insurance fraud means lower insurance premiums for all drivers.

Additionally, all auto insurance rates and policies must be approved by the state’s Department of Financial and Insurance Services before they can be marketed to consumers. New rates and products will be vetted before you purchase them.

Insurance companies, agencies, and licensed insurance agents will see increased fines if they violate the law.

6. Mini-tort reform.

Suppose you go to small claims court for uninsured damages. Michigan’s new law raises the amount of money that you can conceivably recover in such cases.

Visit Michigan’s new auto insurance law website for more information on these policy changes that will take effect in July 2020.

What’s next? Getting the best and cheapest auto insurance quotes in Michigan

Whether you’re in Detroit, Grand Rapid, Marquette, or Kalamazoo, you stand to secure lower auto insurance rates this July.

Many more insurance providers and plans might be accessible to you for the first time. So, where to start shopping around for a new policy?

Go to Insurify, an insurance comparison site, for the fastest, easiest way to compare auto insurance quotes based on your driver profile. Compare ready-to-buy policies from top-rated national and regional companies. Think of it as your personal insurance agent—except now, finally, you’re in the driver’s seat!

Browse, Compare, Discover with Insurify today!